Can We Now Have More Confidence in the eCommerce Market?

)

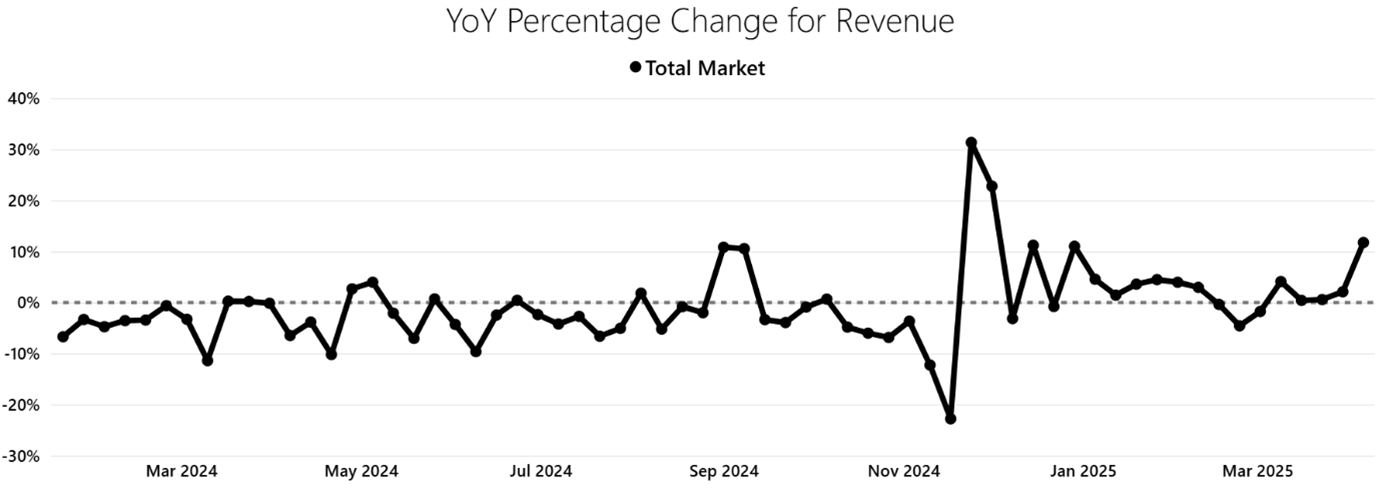

A few months’ ago, in this very series, I posited the idea that eCommerce might be making a bit of a comeback following years in the growth wilderness. The early weeks of the year were all positive for revenue growth, but this was against some quite strong declines for the same period in 2024, so any suggestion that it might be returning to something more reliably positive felt rather tentative.

Here we are though with a few more weeks under 2025’s belt, taking us up to almost a third of the year done, and a strange vision has been popping its head above the waves without sinking straight back down and drowning again moments later; confidence.

This is one of those moments where you almost don’t want to say it out loud, lest it curses the recovery, but the revenue growth line in the below chart from the start of this year has been very solid and reliable compared to where it was in the year previous. In 2024 it was rare to see even two consecutive weeks above the base line, let alone 13 of the first 15.

And those two weeks of negative growth are not the cause for concern that they may first appear. Every year there are significant retail events that move in the calendar, with Mothers’ Day and Easter being two of the major ones. Both of those went back in the calendar by almost three weeks this year compared to 2024, so the decline for growth in March 2025 was actually due to the weeks leading up to Mothers’ Day not aligning and showing a skewed like-for-like.

Likewise, the final week on the graph shows where Easter moved, so the promotional activity that accompanies it produced growth of over 11%; crucially though, the weeks before that when we might have expected a negative impact due to the non-date alignment of Easter did not show a notable decline. This means that, on balance, Easter trading seems to have been pretty good.

To quantify how good trade has been thus far, our forecast for revenue growth in 2025 was +1%; year-to-date, it is running at +2.9%. It is early days still and there is a lot of ground to cover, but you can’t help but feel encouraged by the start the market has made.

Category Winners and Losers: A Mixed Bag Beneath the Surface

It’s not been across all categories the same though. Health & beauty has been buoyant for 18 months now and continues to perform very well, with fragrance a particular standout. Home & garden has been positive for most of 2025 to date, with furniture doing well and garden benefitting from the sunny weather. Electrical has seen some sub-categories selling well while other struggled, but overall it has been more up than down. Pre-orders for the Nintendo Switch 2 seem to have boosted gaming and computing.

On the other side, gifts has been the worst-hit category for a number of years now but even this one has just seen five weeks of consecutive growth for the first time since 2021. Clothing is experiencing the toughest conditions however, with only footwear seeing more positive growth than negative while womenswear and menswear have hardly seen any positive growth all year. The real reasons may be multiple and complex, but it does feel like Vinted might be exerting a good deal of influence here.

It can all turn around, it’s quite possible that the global economy falls into recession this year and the UK might have to navigate a difficult period, but there’s no denying that the ecommerce market is appearing more resilient and reliable than it has done in a long time.

Looking at the above graph, there are plenty of times over the coming months where we will be comparing against negative growth from last year, making it easier and more likely that we can secure growth against those periods. There are some positive weeks to come up against too, so it won’t be growth all the way through and Black Friday did pretty well last year so we won’t stay at +2.9% until the end of the year.

Still, it’s nice to have a buffer. Now that’s confidence for you.

Latest News

-

) Stay up to date with July's biggest ecommerce developments, including BNPL regulation, AI-powered shopping, rapid delivery, marketplace accountability and international selling opportunities.

Stay up to date with July's biggest ecommerce developments, including BNPL regulation, AI-powered shopping, rapid delivery, marketplace accountability and international selling opportunities. -

) The Paypers' Global Ecommerce Report 2026 explores cross-border growth, emerging markets, payments innovation and AI, providing data-driven insights to help businesses succeed in a rapidly evolving ec ...

The Paypers' Global Ecommerce Report 2026 explores cross-border growth, emerging markets, payments innovation and AI, providing data-driven insights to help businesses succeed in a rapidly evolving ec ... -

) April 2026 in eCommerce: AI drives real results, loyalty evolves into lifestyle, and retailers invest in smarter systems to connect channels, improve operations and enhance the customer journey.

April 2026 in eCommerce: AI drives real results, loyalty evolves into lifestyle, and retailers invest in smarter systems to connect channels, improve operations and enhance the customer journey. -

) AI discovery, conversational search, social commerce, loyalty-led marketplaces and faster delivery models show eCommerce shifting toward connected, frictionless journeys across platforms, channels and ...

AI discovery, conversational search, social commerce, loyalty-led marketplaces and faster delivery models show eCommerce shifting toward connected, frictionless journeys across platforms, channels and ... -

) From brand marketing to ecommerce leadership, Leo reflects on experimentation, scaling innovation inside legacy organisations, and building strategy-first ecommerce functions that drive sustainable, d ...

From brand marketing to ecommerce leadership, Leo reflects on experimentation, scaling innovation inside legacy organisations, and building strategy-first ecommerce functions that drive sustainable, d ... -

A concise industry update covering UK eCommerce peak trading trends, forthcoming regulatory changes across subscriptions, digital markets and data privacy, and a B2B case study highlighting evolving p ...

-

) Insights from Ernesto Rojas on career-defining moments, channel strategy, and how AI is reshaping the future of eCommerce.

Insights from Ernesto Rojas on career-defining moments, channel strategy, and how AI is reshaping the future of eCommerce. -

) Retailers face a high-stakes peak trading season shaped by tough comparators, shifting consumer demand, political uncertainty, infrastructure risks, and weather disruptions—hoping favourable condition ...

Retailers face a high-stakes peak trading season shaped by tough comparators, shifting consumer demand, political uncertainty, infrastructure risks, and weather disruptions—hoping favourable condition ... -

) Dave Morrissey, a former Meta and TikTok leader shares career lessons, the future of social commerce, and why creators, speed, and customer-centricity will define the next era of digital retail.

Dave Morrissey, a former Meta and TikTok leader shares career lessons, the future of social commerce, and why creators, speed, and customer-centricity will define the next era of digital retail. -

) AI’s buzz is deafening, but eCommerce is finally turning talk into action. Retailers shift from curiosity to experimentation as genuine automation and personalisation edge closer.

AI’s buzz is deafening, but eCommerce is finally turning talk into action. Retailers shift from curiosity to experimentation as genuine automation and personalisation edge closer. -

) Exploring retail media, AI-powered workflows, and eCommerce scaling challenges ahead of peak season—insights on opportunities, innovation, and collaboration from eCommerce Expo and Technology for Mark ...

Exploring retail media, AI-powered workflows, and eCommerce scaling challenges ahead of peak season—insights on opportunities, innovation, and collaboration from eCommerce Expo and Technology for Mark ... -

) Linnworks discusses AI hype, peak season readiness, and global marketplace opportunities, plus a session on how retailers can scale from £10 to £10M by embracing diversification and resilience.

Linnworks discusses AI hype, peak season readiness, and global marketplace opportunities, plus a session on how retailers can scale from £10 to £10M by embracing diversification and resilience. -

) Klaviyo explores AI personalisation, retention, and community-driven commerce, plus a session on how brands like Wild are turning customers into loyal advocates through personalised experiences.

Klaviyo explores AI personalisation, retention, and community-driven commerce, plus a session on how brands like Wild are turning customers into loyal advocates through personalised experiences. -

) Mapp explores how enriched product data unlocks discovery, cashflow, and margin gains, plus a session on why structured attribution is reshaping the future of retail.

Mapp explores how enriched product data unlocks discovery, cashflow, and margin gains, plus a session on why structured attribution is reshaping the future of retail. -

) Marketing compliance is emerging as a competitive advantage in e-commerce, helping brands build trust, avoid costly penalties, protect platform presence, and future-proof growth by aligning with evolv ...

Marketing compliance is emerging as a competitive advantage in e-commerce, helping brands build trust, avoid costly penalties, protect platform presence, and future-proof growth by aligning with evolv ... -

) Woo + Pressable share insights on ecommerce trends, peak season challenges, and the customer-centric innovations redefining digital commerce, plus a preview of their session on shifting shopper behavi ...

Woo + Pressable share insights on ecommerce trends, peak season challenges, and the customer-centric innovations redefining digital commerce, plus a preview of their session on shifting shopper behavi ... -

) Exploring AI adoption, evolving loyalty, and sustained peak season strategies, this perspective highlights how brands can stand out by staying curious and customer-focused in a fast-changing ecommerce ...

Exploring AI adoption, evolving loyalty, and sustained peak season strategies, this perspective highlights how brands can stand out by staying curious and customer-focused in a fast-changing ecommerce ... -

) Propeller Group’s Alex Humphries-French shares how exhibitors can cut through the noise at industry events with smarter PR—shaping stories, engaging media, and building lasting visibility before, duri ...

Propeller Group’s Alex Humphries-French shares how exhibitors can cut through the noise at industry events with smarter PR—shaping stories, engaging media, and building lasting visibility before, duri ... -

) Nova Tissue transformed its business with Temu, unlocking rapid e-commerce growth, boosting profitability, and creating jobs — all while navigating rising costs and shrinking traditional sales channel ...

Nova Tissue transformed its business with Temu, unlocking rapid e-commerce growth, boosting profitability, and creating jobs — all while navigating rising costs and shrinking traditional sales channel ... -

) AI-driven personalization, economic uncertainty, and evolving consumer expectations are reshaping eCommerce. Ahead of eCommerce Expo 2025, discover insights on resilience, continuous learning, and why ...

AI-driven personalization, economic uncertainty, and evolving consumer expectations are reshaping eCommerce. Ahead of eCommerce Expo 2025, discover insights on resilience, continuous learning, and why ... -

) Bluestone PIM explores how AI personalization, composable commerce, and product experience management are reshaping eCommerce. From data challenges to omnichannel growth, discover insights, advice, an ...

Bluestone PIM explores how AI personalization, composable commerce, and product experience management are reshaping eCommerce. From data challenges to omnichannel growth, discover insights, advice, an ... -

) Gavin Holland, Global Head of UX Design at JD Sports Fashion, reflects on his career journey from BBC Worldwide to leading global UX at scale. He shares insights on collaboration, personalisation, AI- ...

Gavin Holland, Global Head of UX Design at JD Sports Fashion, reflects on his career journey from BBC Worldwide to leading global UX at scale. He shares insights on collaboration, personalisation, AI- ... -

) From bricks-and-mortar to digital transformation, this interview explores the evolving world of ecommerce trading at Primark, touching on performance metrics, stock strategy, and the customer-centric ...

From bricks-and-mortar to digital transformation, this interview explores the evolving world of ecommerce trading at Primark, touching on performance metrics, stock strategy, and the customer-centric ... -

) Despite Britain’s unpredictable weather, seasonal shifts significantly impact retail. While heatwaves drive demand in categories like appliances and outdoor gear, clothing sales remain sluggish due to ...

Despite Britain’s unpredictable weather, seasonal shifts significantly impact retail. While heatwaves drive demand in categories like appliances and outdoor gear, clothing sales remain sluggish due to ... -

) Our media partner, The Paypers, has launched the Global Ecommerce Report 2025, teaming up with industry experts to bring you a guide to global expansion packed with insights to help you succeed.

Our media partner, The Paypers, has launched the Global Ecommerce Report 2025, teaming up with industry experts to bring you a guide to global expansion packed with insights to help you succeed. -

) In eCommerce performance analysis, averages are essential — but they can also be deceptive. This article explores the limitations of relying solely on average figures, particularly in benchmarking sce ...

In eCommerce performance analysis, averages are essential — but they can also be deceptive. This article explores the limitations of relying solely on average figures, particularly in benchmarking sce ... -

) From Walmart’s tariff-driven pricing backlash to Tesco’s leadership shakeup and Shein’s IPO detour, May saw pivotal changes across global retail. AI disruption, influencer marketing growth, and rising ...

From Walmart’s tariff-driven pricing backlash to Tesco’s leadership shakeup and Shein’s IPO detour, May saw pivotal changes across global retail. AI disruption, influencer marketing growth, and rising ... -

) Growth Summit 2025 is officially open for registration. This new invite-only experience is designed for senior retail leaders who want to sharpen their strategy, connect with peers, and benchmark thei ...

Growth Summit 2025 is officially open for registration. This new invite-only experience is designed for senior retail leaders who want to sharpen their strategy, connect with peers, and benchmark thei ... -

) After such a long period of decline for the eCommerce market, where any positive growth gain made in one week would quickly be eliminated by a drop over the subsequent weeks, we can perhaps be forgive ...

After such a long period of decline for the eCommerce market, where any positive growth gain made in one week would quickly be eliminated by a drop over the subsequent weeks, we can perhaps be forgive ... -

) Currently UX Research Manager at Tesco, Serkan Ayan shares how human-centred research drives customer experience, how to scale UX in large organisations, and why curiosity is key to career growth in t ...

Currently UX Research Manager at Tesco, Serkan Ayan shares how human-centred research drives customer experience, how to scale UX in large organisations, and why curiosity is key to career growth in t ...

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)

)